What’s KYC and why is it so difficult?

At its most simple, Know Your Buyer (KYC) is a due diligence course of used to confirm that the individual is who they are saying they’re and that knowledge they’ve shared is appropriate (e.g. cellphone quantity, e-mail, and deal with). KYC rules are in place to forestall felony actions corresponding to identification fraud, cash laundering, and different monetary crimes. Nevertheless, the compliance and implementation of those rules comes with a number of challenges. A few of these challenges embody:

- Buyer identification: You’ll want to check the client’s likeness with a photograph on an authorised ID card (normally government-issued like a passport or driver’s license). There’s further friction if this occurs in-person.

- Documentation verification: Ensuring the image matches the individual isn’t sufficient; the government-issued ID of the person should be checked for forgery or tampering. This requires the individual finishing up the verification to be educated to acknowledge these indicators and search for the presence of acceptable watermarks, and so on.

- Deal with verification: As a further test on their paperwork, the client should present proof that they dwell on the deal with on the government-issued ID paperwork (Proof of Deal with or POA) normally by offering current utility payments. That is getting trickier as many people go for digital payments, so the client might need to request one-off letters from authorised sources to show they dwell on the deal with they’ve supplied.

- Confirm contact particulars: Lastly, you’ll have to test that the e-mail deal with and cellphone quantity supplied are appropriate and belong to the client. A standard method is to help a one-time-passcode (OTP) system that permits a buyer to enter the passcode they obtain and have it linked to the account profile that’s being created.

For software program builders, all of those steps decelerate your consumer onboarding. Many of those verification steps are handbook and a few require the client to come back in to satisfy face-to-face, which provides friction to the onboarding expertise. This handbook course of creates further prices for the group performing the validations.

KYC can have a number of layers of buyer verification corresponding to anti-money laundering checks and danger assessments—for instance, utilizing Ekata to identify if an deal with supplied has getting used repeatedly earlier than for fraudulent transactions. It might probably even embody checking a person’s crypto footprint for inappropriate transaction historical past or in the event that they’re on a sanctions checklist (Ciphertrace).

For the needs of this submit, we’re going to have a look at how Mastercard Open Banking Account Proprietor Verification APIs might help help probably the most basic step in a KYC pipeline: confirm the digital identification of your customers or small companies based mostly on their supplied identify, deal with, and make contact with particulars.

However the banks have already completed KYC for his or her clients!

Sure, the banks have constructed a rigorous KYC observe to confirm clients earlier than they open any account. Banks adhere to a variety of regional privateness, safety, and anti-money laundering rules. Many people have needed to undergo that strategy of offering proof of identification and deal with in addition to finishing registrations utilizing OTPs despatched to our e-mail and cellphone. An essential consideration is how we as clients additionally preserve this data updated, so we don’t miss any essential communications from our financial institution.

The timeliness, high quality, and accuracy of the client knowledge that the financial institution holds could be very helpful, but in addition invaluable due to the effort and time invested in gathering it and protecting it updated. The US Open Banking API lets you unlock this worth. Particularly, we are able to use the Account Proprietor Verification API to entry this invaluable knowledge.

Utilizing Mastercard Account Proprietor Verification APIs to leverage the financial institution’s KYC efforts

Open banking empowers customers (customers and small companies) to entry, use, and profit from their very own monetary knowledge. They’ll management what accounts could be seen, how lengthy that entry could be granted, and for what objective— issues like opening new accounts, securing loans, bettering credit score scores, and enabling client selection in funds.

The consumer (your buyer) feels protected doing this as a result of they’re authenticating instantly with their financial institution utilizing their on-line banking credentials, giving them confidence that the third-party received’t see or retailer them.

The US Open Banking API handles a trusted connections to the banks, gives a safe dialog so the account holder can authenticate, and caches the monetary knowledge so if you execute a question it comes again rapidly (avoiding a spherical journey to the financial institution each time).

The US Open Banking API gives a variety of options together with account aggregation, cost enablement, and confidence scores that can be utilized for monetary companies use circumstances like lending, funds, and account opening.

To assist help your KYC pipeline, we are able to use Mastercard’s Account Proprietor Verification API, which returns financial institution pre-verified knowledge (i.e. identify, e-mail, deal with and cellphone quantity) together with identification insights and an identification danger rating based mostly on customers’ exercise sample and its affiliation to assist detect fraudulent conduct, thereby immediately verifying that the consumer (checking account homeowners) are real and assist mitigate on-line fraud. This makes it exponentially more durable for criminals to make use of actual or pretend IDs to commit fraud and considerably reduces identification fraud by enhancing the effectiveness of fraud detection techniques for account openings, me-to-me (M2M) transfers, peer-to-peer (P2P) transfers, invoice funds, and different transactions.

The way it works

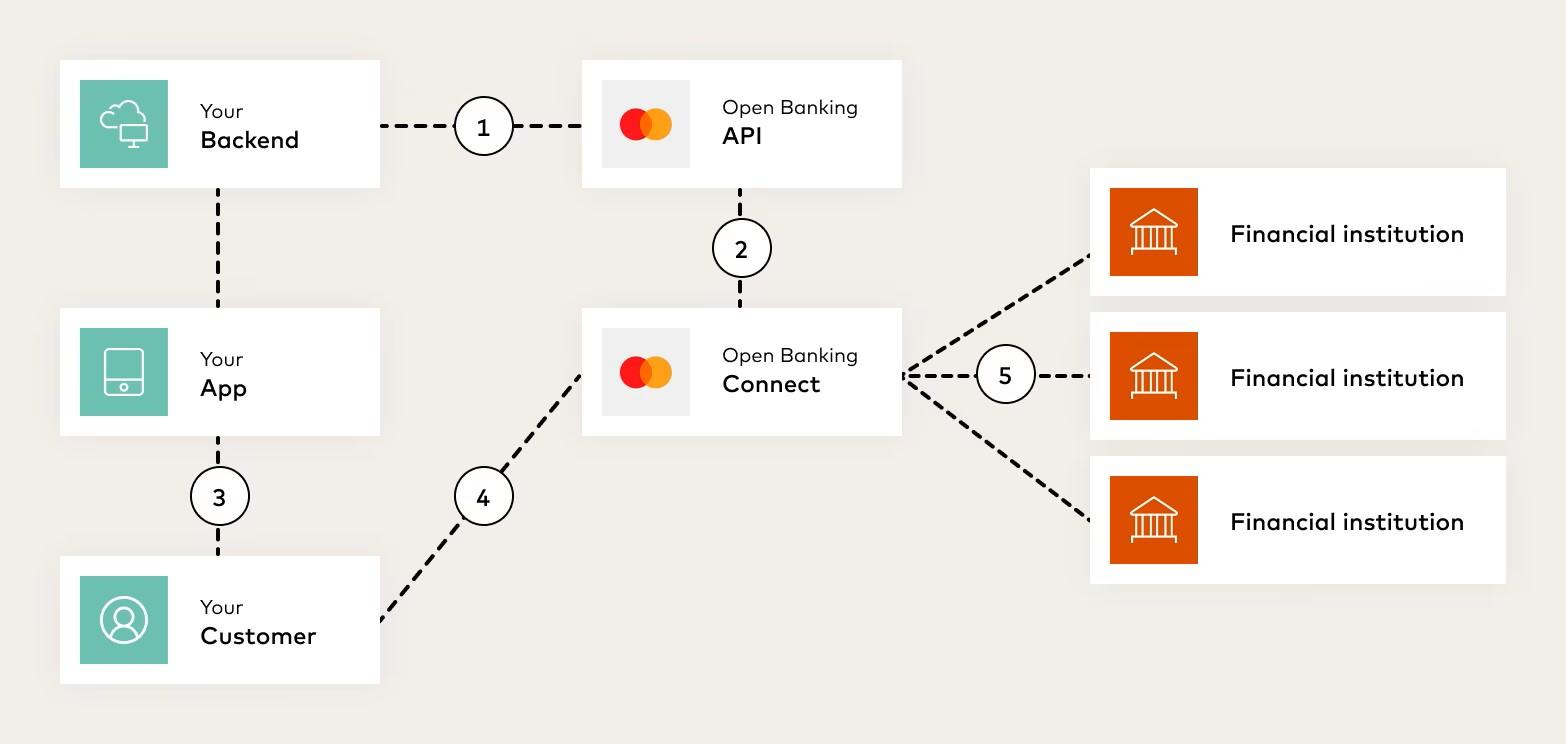

- Your server registers a buyer with Open Banking and receives an ID for this buyer.

- With this buyer ID, your server can generate a redirect URL for loading the join expertise that can enable the client to hook up with their financial institution.

- Your frontend software redirects the client to attach utilizing the generated URL from step 2.

- The shopper logs into their monetary establishment utilizing their financial institution credentials by way of the join expertise.

- The shopper grants permission for his or her monetary knowledge to be accessed.

As soon as the client has granted you entry to the account, you make a name to the Get Account Proprietor Particulars API.

The Get Account Proprietor Particulars API is aligned with the Monetary Information Change (FDX) requirements. The FDX is devoted to unifying requirements for safe and handy entry of user-permissioned monetary knowledge sharing all through the monetary companies trade. This enables the API to return the payload concerning the consumer (client or small enterprise) in an ordinary format with the next particulars:

- Names: The names of the account holders. It’s going to additionally point out whether or not it’s a individual, enterprise, or different entity.

- Deal with: The usual format for a US deal with, damaged into constituent elements, which may even have an entry to say if it’s a enterprise or residence deal with.

- Telephone numbers: An array of contact cellphone numbers together with sort (Private/Enterprise).

- Electronic mail addresses: An array of e-mail addresses and their sort (Private/Enterprise).

- Documentation: An array of the doc proofs supplied: tax identifier SSN, government-issued ID (passport quantity, visa quantity, driver’s license quantity, and so on.) Fast sidebar: although this ingredient is a required area in some areas, it’s not necessary within the US, and as such, it’s on the discretion of the financial institution.

Instance response

{

"holders": [

{

"relationship": "AUTHORIZED_USER",

"ownerName": "John Smith, PhD",

"firstName": "John",

"middleName": "L",

"lastName": "Smith",

"suffix": "PhD",

"nameClassification": "person",

"nameClassificationconfidencescore": 100,

"addresses": [

{

"ownerAddress": "434 W Ascension Way",

"type": "Home",

"line1": "434 W Ascension Way",

"line2": "Suite #200",

"line3": "UT 84123",

"city": "Murray",

"state": "UT",

"postalCode": "84123",

"country": "USA"

}

],

"emails": [

{

"isPrimary": true,

"email": "myname@mycompany.com",

"emailType": "Personal"

}

],

"telephones": [

{

"type": "HOME",

"country": "61",

"phone": "1-801-984-4200"

}

],

"documentations": [

{

"taxId": "123-45-7890",

"taxIdCountry": "USA",

"governmentId": "123456789"

}

]

}

]

}

Congratulations! Now you’ve the information (verified by a financial institution) mandatory to reinforce your buyer onboarding course of.

How are the account holder’s credentials secured?

The US Open Banking Service makes use of OAuth when integrating into the financial institution APIs and as a 3rd celebration in that course of, it by no means sees the account holder credentials. When the account holder efficiently authenticates with their financial institution and selects the account they wish to enable entry to and for the way lengthy, the service will get a token that it encrypts and shops till it must entry the information. It is going to be restricted to simply the information that the account holder has explicitly granted entry to.

If you’re utilizing the Get Account Proprietor Particulars API as a part of a one-off buyer onboarding verification step, you possibly can set the token as much as be a single-use token to additional restrict entry to the account proprietor knowledge. If, nonetheless, it’s a part of a broader Account Opening course of, Account Aggregation or comparable Open Banking use case, you possibly can configure the token to dwell for an extended time frame.

How do I get began?

Try this Fast Begin Information on Mastercard Builders to stand up and working with the US Open Banking API after which use the Get Account Proprietor Particulars API name to tug the information essential to energy your KYC course of.

Tags: api, fintech, open banking, associate content material, partnercontent

{kind=link}