TSMC’s income this yr goes to set an all-time file for the corporate, because of excessive demand for chips in addition to elevated costs that its prospects are prepared to pay for its providers. Whereas the corporate admits that demand for chips geared toward client units is slowing, demand for 5G, AI, HPC, and automotive chips stays regular. In actual fact, TSMC’s foremost drawback at current is getting extra fab tools, as ASML and different instrument companies and reporting that demand for semiconductor manufacturing instruments considerably exceeds provide.

Final week TSMC posted its monetary outcomes for the second quarter of 2022. The corporate’s income hit a file $18.2 billion, which was a year-over-year enhance of 43.5%. The corporate revealed that whereas its gross sales had been up 55% and 65.3% in April and Might (respectively), its income in June was ‘solely’ up 18.5% YoY, which signifies a slowdown in gross sales progress.

Demand for Consumer Gadgets Slowing

“Because of the softening system momentum in smartphone, PC and client finish market segments, we observe the provision chain is already taking motion and anticipate stock degree to scale back all through the second half 2022,” stated C.C. Wei, chief govt of TSMC, on the firm’s earnings convention name.

Whereas we are able to solely speculate on this, it appears like a few of TSMC’s prospects lowered their orders for client-oriented chips after Russia began a full-scale battle towards Ukraine in late February. TSMC expenses/acknowledges income when it delivers chips/wafers to a shopper.

Manufacturing cycle for chips on fashionable course of applied sciences is properly over 60 days relying on complexity and the variety of layers: N16 is ~60 days, N7 is 90+ days, N5 might be properly over 100 days. These nodes account for 65% of TSMC’s income. So, if purchasers began to wind down orders in March and April as they anticipated rising inflation and uncertainty among the many finish consumer, the impact will likely be seen in June, which is what might be noticed in TSMC’s stories.

TSMC admits that demand for client-oriented chips is softening, however demand for chips designed to help 5G, AI, and HPC functions nonetheless exceeds the corporate’s skills to provide.

“Whereas we observe softness in client finish market segments, different finish market segments corresponding to information heart and automotive-related stay regular,” stated Wei. “We’re capable of reallocate our capability to help these areas. Regardless of the continued stock correction, our prospects’ demand continues to exceed our capability to provide. We anticipate our capability to stay tight all through 2022 and our full yr progress to be mid-30% in U.S. greenback phrases.”

Superior Nodes to Stay Development Drivers, Expansions Getting Harder

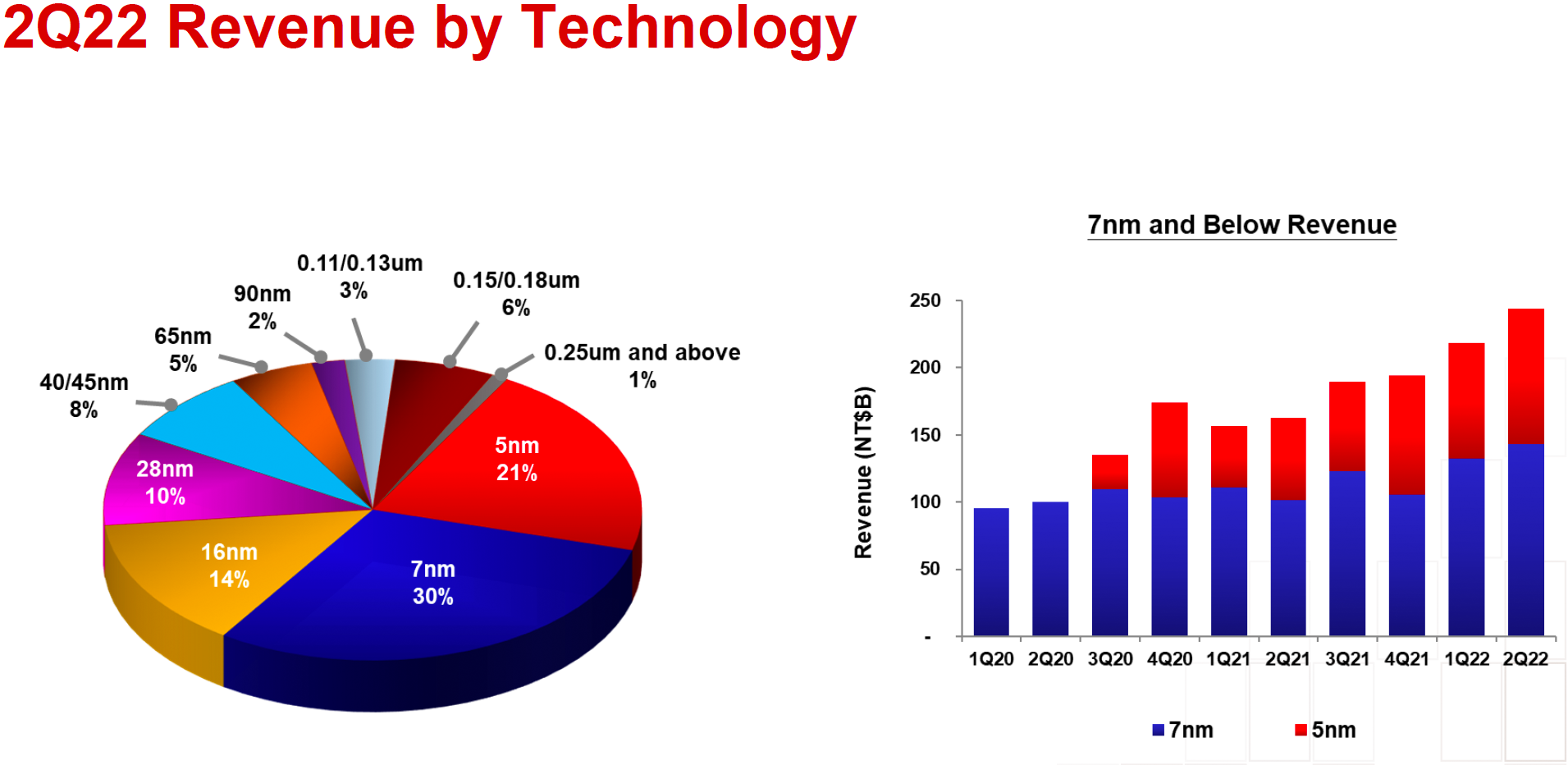

Over half of TSMC’s income (51%) comes from chips made utilizing its superior fabrication applied sciences (N7 and thinner nodes), which isn’t significantly shocking as TSMC is likely one of the solely two contract foundries that supply such subtle manufacturing processes to purchasers.

These applied sciences will likely be amongst TSMC’s foremost progress drivers within the coming years, particularly as extra prospects undertake N7 and extra superior applied sciences. However extra N7/N6 and N5/N4 orders imply that TSMC might want to construct extra capability for these nodes, in addition to extra capability for N3 and subsequent nodes, which is why the corporate estimated that its CapEx this yr would attain $40 billion – $44 billion.

“With the profitable ramp of N5, N4P, N4X, and the upcoming ramp-up of N3, we are going to broaden our buyer product portfolio and enhance our addressable market,” stated the top of TSMC. “The macroeconomic uncertainty might persist into 2023, our know-how management will proceed to advance and help our progress. […] We consider the basic structural progress trajectory within the long-term semiconductor demand stays firmly in place. “

The world’s No. 1 contract maker of semiconductors additionally urges prospects to migrate from older nodes to 28nm and specialty applied sciences as this may guarantee capability availability (as TSMC plans to broaden capability for 28 nm and specialty nodes by 50% by 2025) and denser designs doubtlessly with extra options.

Constructing extra modern, 28 nm, and specialty capacities not solely requires huge investments, however TSMC wants to acquire extra semiconductor manufacturing instruments. Whether or not TSMC is constructing capacities for its brand-new N3 node or 28nm/specialty applied sciences, it ought to be famous that the corporate wants every kind of lithography machines for them. An N3-capable fab wants dry litho instruments, immersion litho scanners, and EUV-capable tools. With out required variety of dry and immersion scanners, a sophisticated EUV machine by itself will likely be ineffective. In the meantime, lithography instruments are usually not the one equipment {that a} fab wants.

Apparently, demand for fab tools is so excessive that TSMC will be unable to spend its CapEx price range this yr, and a few purchases associated to superior (N7 and thinner) and mature nodes will likely be delayed into 2023. Consequently, TSMC’s CapEx this yr will likely be at a decrease finish of the corporate’s prediction (round $40 billion) not as a result of it doesn’t need to make investments, however as a result of it can not spend money on instruments that aren’t obtainable.

“Our suppliers have been dealing with better challenges of their provide chains, that are extending instrument supply lead instances for each superior and mature nodes,” stated Wei. “Consequently, we anticipate a few of our CapEx this yr to be pushed out into 2023.”

ASML Confirms Report Quarterly Bookings

In the meantime, ASML, the world’s largest producer of lithography instruments, this week posted its Q2 2022 income of €5.431 billion, a 53% enhance year-over-year. Through the second quarter, the corporate equipped (acknowledged income) a complete of 91 new lithography programs (up from 59 in Q2 2021), with 12 of these being EUV programs (up from 3 in Q2 2021).

What is probably extra necessary is that ASML’s web bookings for brand spanking new programs totaled €8.461 billion through the quarter, so the corporate’s bookings are greater than its quarterly gross sales. In the meantime, ASML’s backlog now totals €33 billion and spans a number of years to come back, which primarily is a one more affirmation that this can be very exhausting for corporations like TSMC to get new instruments.

The backlog for DUV machines is now at round 600 items and product order lead time for a brand new DUV scanner is now about two years. The backlog for EUV instruments is properly over 100 machines. In the meantime, ASML says that PO lead time metrics will not be precisely related because it faces provide chain and personal manufacturing capability points, which implies that its companions should construct extra capability and ASML has to construct extra capability (which takes time) and solely then it will likely be capable of provide the instruments ordered just lately.

For the entire yr 2022, ASML expects to ship 55 excessive ultraviolet (EUV) lithography scanners, however acknowledge income of 40 EUV programs valued at €6.40 billion (€160/$140 million per machine) as a result of 15 EUV machines will likely be so-called quick shipments — a cargo course of that skips a few of the testing at ASML’s manufacturing unit after which closing testing and formal acceptance are carried out on the buyer web site (which is why income acceptance will get deferred). The corporate additionally intends to provide 240 deep ultraviolet (DUV) litho instruments this yr. ASML expects its manufacturing capability to whole 60 EUV scanners and 375+ DUV instruments in 2023.

Abstract

Whereas demand for chips geared toward shopper/client units is getting softer attributable to rising inflation and geopolitical uncertainty, the worldwide megatrends like 5G, AI, HPC, and autonomous automobiles are nonetheless there and these require a great deal of superior system-on-chips, specialty processors, and not-so-advanced issues like sensors. Subsequently, TSMC is assured of robust demand for chips within the coming years.

However there’s a drawback with assembly that demand as TSMC will not be the one firm that’s increasing its manufacturing capability. ASML’s backlog now contains over 100 EUV scanners and round 600 DUV scanners — it’s going to take years for the corporate to ship these machines. Consequently, TSMC has issues with acquiring instruments it must construct extra capability it wants. It’s unclear whether or not the corporate has sufficient capability to fulfill the entire potential demand from its largest prospects on N3, N4, N5 nodes (Apple, MediaTek, AMD, NVIDIA, and so on.), however, in the end, instrument shortages will have an effect on all of its course of applied sciences.

{kind=link}